Are you looking for information about inheritance tax in Catalonia? Whether you are looking to learn more about inheritance tax in Barcelona or in Catalonia in general, here are some keys so you can get a good understanding of this tax and all that surrounds it.

When a loved one passes away the last thing you want to want to think about is any administrative issue. Unfortunately there are many things to consider. With regards to any tax due on receiving an inheritance, forward planning and a clear understanding of how inheritance tax is calculated can help to ease some of the stress when it comes to fiscal concerns.

Who is obliged to pay Inheritance Tax in Catalonia?

The person obliged to pay inheritance tax in Spain is the person receiving the inheritance, the beneficiary, not the person who has passed away. This is different to the situation in the UK where the inheritance tax is paid by the ‘estate’, not the beneficiary.

In Catalonia the beneficiary is obliged to pay inheritance tax in the following cases:

– If the deceased had their habitual residence in Catalonia then the beneficiary must pay inheritance tax in Catalonia regardless of their place of residence

– If the beneficiary is resident in Catalonia then they must pay inheritance tax in Catalonia regardless of the place of residence of the deceased

– If a property inherited is situated in Catalonia then the beneficiary must pay inheritance tax in Catalonia regardless of their place of residence

There are certain deductions and discounts that can reduce the amount of tax due, and these vary between the autonomous communities. The inheritance tax must be declared within six months of the death, although an extension of an additional six months can be requested in the first five months after the death.

Discover the art of refined living with Bcn Advisors, your trusted partner in luxury real estate, offering a curated selection of luxury apartments for sale in Barcelona tailored to your unique preferences and lifestyle.

How much is Inheritance Tax in Catalonia?

Before the tax due can be calculated there are substantial deductions that can be made to reduce the taxable base. These deductions depend on the degree of kinship with the deceased, the groups being as follows:

Group I

Children, including adopted children, under the age of 21

Group II

Children over 21, spouses, grandchildren, parents

Group III

close relatives, such as brothers, sisters, uncles and aunts

Group IV

more distant relatives or unrelated

The deductions in Catalonia are as follows:

Group I

€100,000 plus €12,000 for each year under 21 years of age, up to €196,000

Group II

child €100,000; spouse €100,000; other descendants €50,000; parents €30,000

Group III

€8,000

Group IV

No deductions available

Deductions are also available in the following situations:

Disabled Beneficiary

In the case where the beneficiary is disabled, an additional deduction of €275,000 is applicable if the disability is determined to be greater than 33%, or €650,000 when it is greater than 65%.

Beneficiary over 75 years old

When the beneficiary belongs to Group II and is over 75, a deduction of €275,000 may be applied. This deduction is applied instead of the other deductions stated above.

Family Home

If a property inherited is the main residence, then a reduction of 95% of the value of the property (up to €500,000) may be applied when the beneficiary is the spouse, child or parent of the deceased, as well as a collateral relative, older than 65, who lived with the deceased during the two years prior to their death. If this reduction is applied then the property may not be sold for a period of five years.

Family Business

A tax deduction of 95% of the net value of the interest held in the business by the deceased is applicable for all beneficiaries up to a third-degree relative, as well as those who are not related but have been employed in the business for at least ten years.

Life Insurance Policies

When the beneficiary is a spouse, descendant or parent of the deceased, then a 100% reduction is applicable on any income from a life insurance policy held by the deceased, up to a maximum of €25,000.

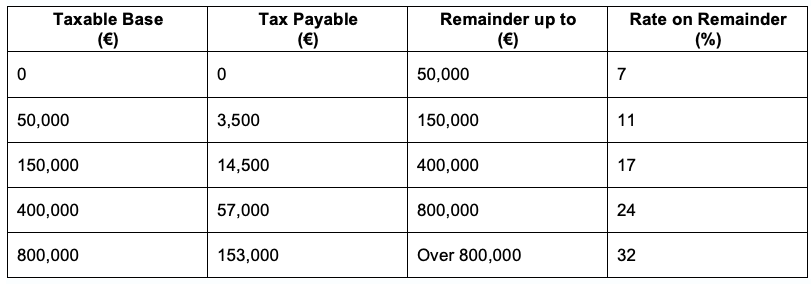

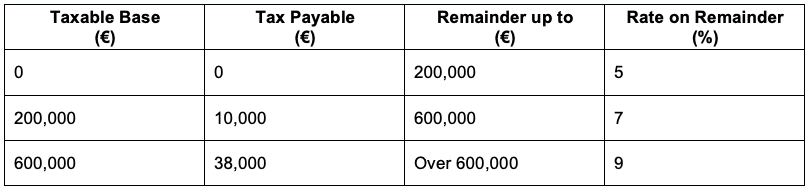

Once the deductions have been applied then the following tax rates are applied:

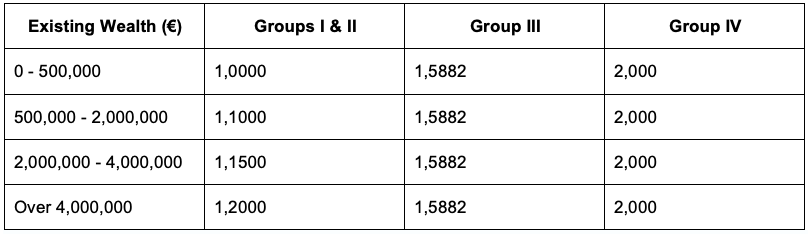

Once the relevant tax has been calculated the result is then multiplied by a coefficient determined by the existing wealth of the beneficiary, as well as the group to which they belong:

There are still further reductions to be made before the final amount of tax due is calculated.

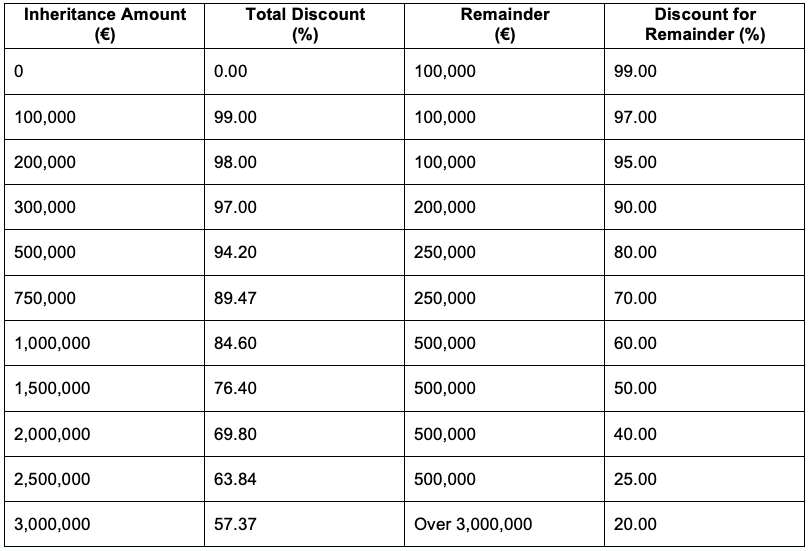

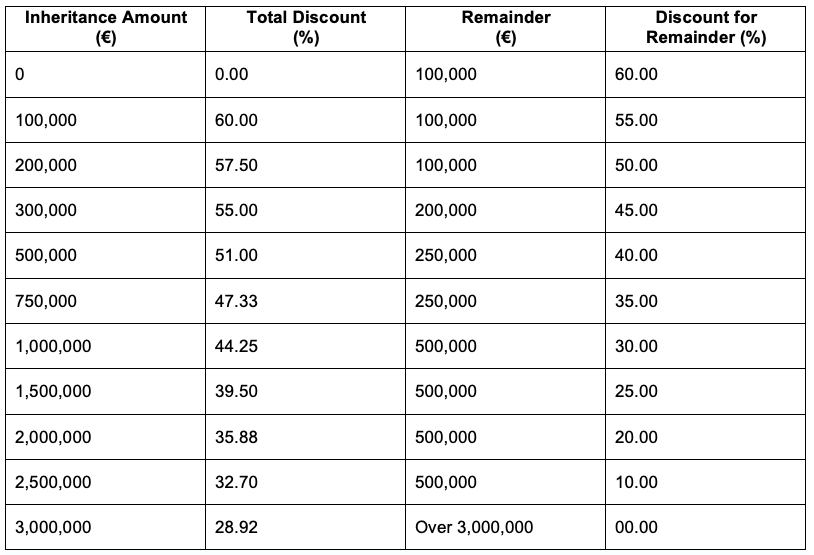

Spouses receive a discount of 99% on any tax payable. For beneficiaries within Groups I and II (not including spouses), the following discounts are applicable:

Group I

Group II

The above discounts are reduced by 50% should the beneficiary apply any of the deductions stated above, with the exception of the deduction applicable to the main residence.

Gift Tax versus Inheritance Tax

In certain cases, it might prove beneficial for a person to donate their assets to their descendants during their lifetime. Whilst the gift tax rates are similar to the inheritance tax rates, it is important to take into consideration that there is a reduced rate when the beneficiary belongs to either Group I or Group II. In order for this reduced rate to be applied the gift must be registered as a public deed before a Notary. The tax rates applicable are then as follows:

Please note that the information in this article is a guide only. A qualified tax lawyer should be used for specific advice.

You may also be interested in...

The 10 best luxury penthouses in Barcelona

Looking for a luxury penthouse in Barcelona? Buying a property of these characteristics means being able to enjoy a high standing home in one of the most avant-garde and dynamic cities in Europe. That is why, from BCN Advisors, we bring you a list of the best luxury penthouses for sale in Barcelona.

Read more

How to Sell a Flat in Sarrià: A Guide for Property Owners

Selling a flat in Sarrià, one of the most exclusive and residential neighbourhoods in Barcelona, is an incredible opportunity to achieve excellent profitability. With its peaceful atmosphere, prestigious international schools, and outstanding quality of life, Sarrià attracts both national and intern

Read more

The new capital gains tax in Spain

Sellers have always known that selling a home involves various costs that impact the final profit from the sale. These expenses include real estate agency fees, legal fees, and mortgage cancellation fees, along with several often-overlooked smaller administrative costs. These might encompass fees fo

Read more